SMM May 30 Report:

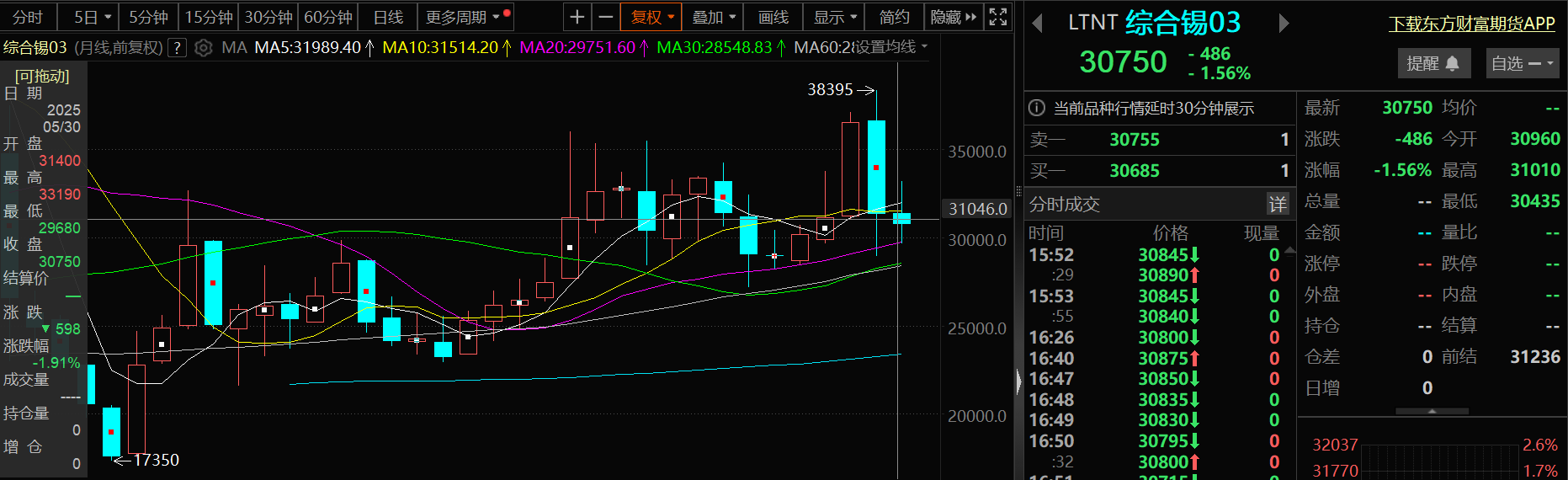

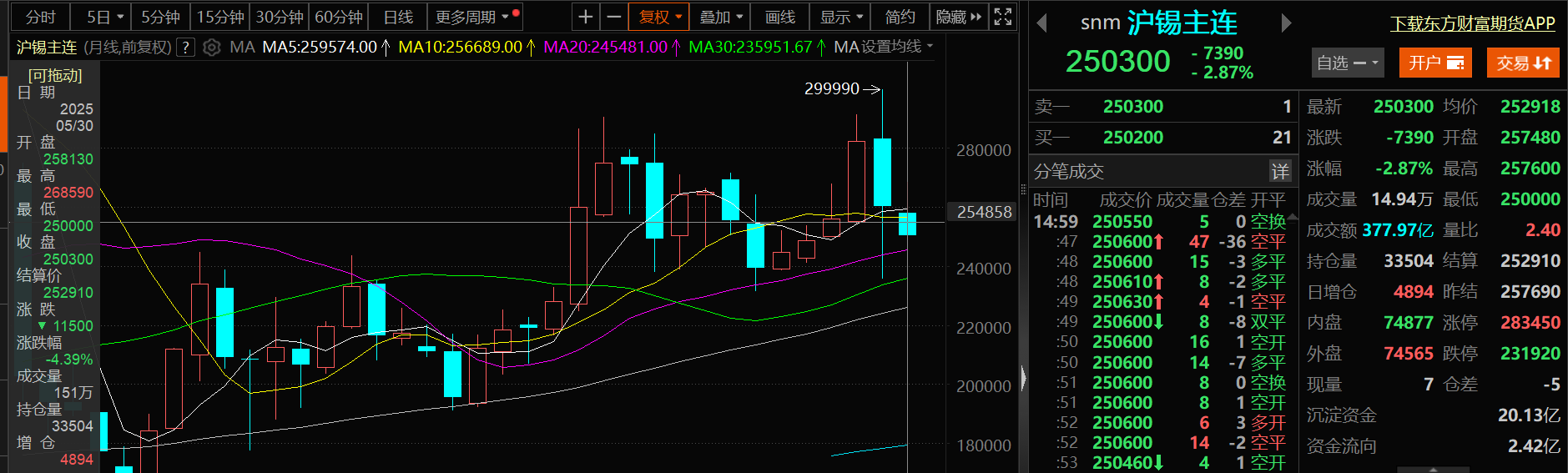

Unlike the significant decline in tin prices in April, tin prices fluctuated rangebound in May. As May drew to a close, despite the ongoing tight supply of tin ore in the short term, market expectations for supply recovery increased due to the gradual resumption of production at tin mines in Myanmar's Wa region and the Democratic Republic of the Congo (DRC). Additionally, the uncertainty surrounding the US tariff policy cooled market risk appetite, leading to a notable correction in tin prices. As of around 18:10 on May 30, LME tin fell by 1.56%, trading at $30,750/mt, with its monthly line for May temporarily down 1.91%; SHFE tin dropped by 2.87%, trading at 250,300 yuan/mt, with its monthly line for May down 4.39%.

》Click to view SMM Futures Data Dashboard

On the spot market

Tin spot prices fell by 3.71% in May

》Subscribe to view SMM Metal Spot Historical Prices

In terms of tin spot prices: According to SMM quotes, the average price of SMM Grade 1 tin spot on May 30 was 251,500 yuan/mt, a decrease of 9,700 yuan/mt compared to the average price of 261,200 yuan/mt on April 30, representing a decline of 3.71%.

Fundamentals

Refined tin production in May decreased by 2.37% MoM

►Production:

According to SMM's data based on market communication and processing, in May 2025, China's refined tin production decreased by 2.37% MoM. On a YoY basis, production fell by 11.24%. The continuous tightening of the tin concentrate and scrap tin supply chains imposed rigid constraints on capacity, leading to a slight decline in the overall operating rate. By region: Yunnan region: A combination of raw material shortages and cost pressures; Jiangxi region: The scrap recycling system is under pressure, with an increased risk of capacity exits;Inner Mongolia, Anhui, and other regions: In Inner Mongolia, production slightly rebounded in May due to production issues at captive mines, but it has not yet returned to previous levels. In Anhui and other producing regions, due to shortages of scrap and tin concentrates, the operating rate continued to fall short of expectations. 》Click to view details

►Operating rate

According to SMM's market survey and processing data, as of Friday this week, the operating rates of refined tin smelters in Yunnan and Jiangxi, the two major tin-producing provinces, remained low, with a combined rate of 54.58%. Among them, the operating rate of smelters in Yunnan slightly declined compared to the previous week and was nearly 10 percentage points lower than at the beginning of the year. Some smelters in core producing areas such as Gejiu have entered seasonal maintenance or production cuts due to raw material shortages and cost pressures. Currently, the raw material inventory of enterprises is generally below 30 days. Some enterprises are facing inventory backlogs due to high-priced stockpiling in the early stage (with a psychological price level of approximately 270,000 yuan/mt), coupled with weak purchase willingness downstream, resulting in significant shipping pressure. Meanwhile, the treatment charges (TCs) for tin concentrates with a 40% grade have remained at historically low levels, approaching the cost line of smelters and severely squeezing profit margins. During the same period, the operating rate of smelters in Jiangxi was only 41.02%, consistently lower than that in Yunnan, and had decreased by approximately 15 percentage points compared to the beginning of the year. Some enterprises were forced to implement long-term production cuts due to insufficient scrap supply, with some production capacity facing the risk of permanent exit.

►Inventory:

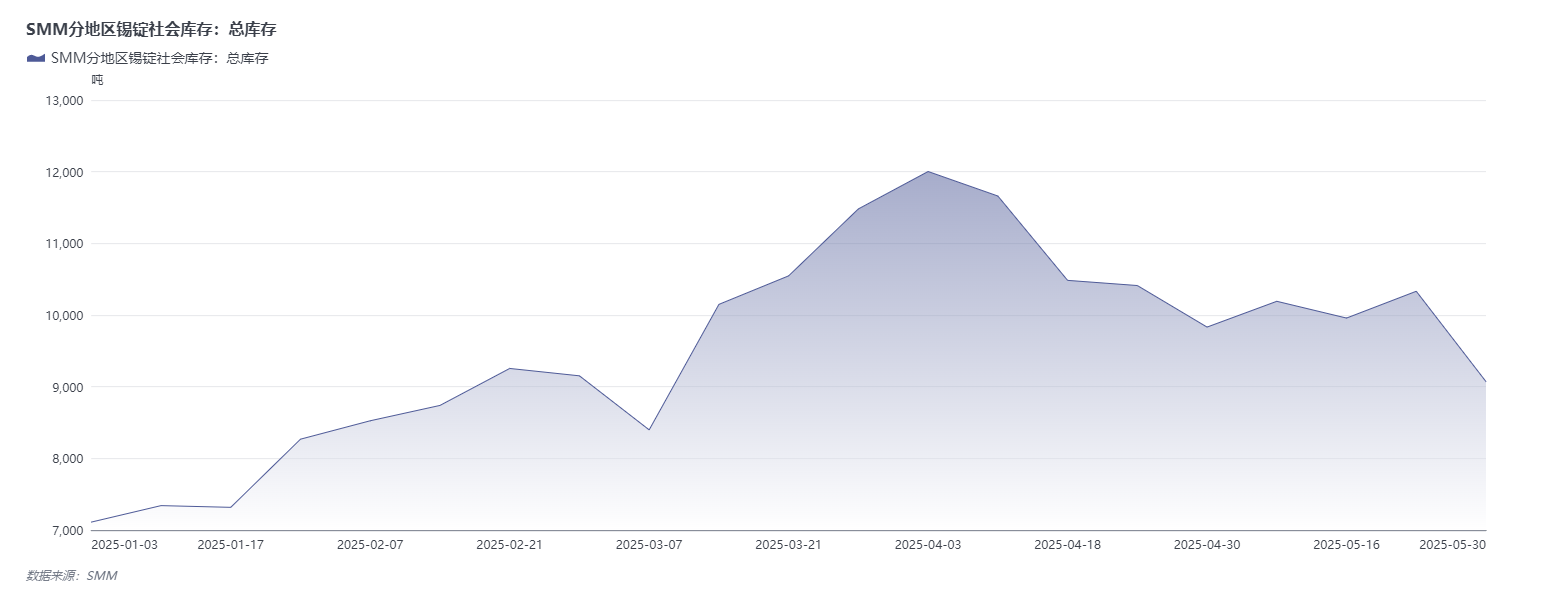

Social inventory of tin ingots across three locations tracked by SMM has declined.

Click to view the SMM tin industry chain database.

Domestic social inventory of tin ingots: This week, SHFE tin prices initially stabilized before falling, with a significant correction during the week. The trigger: Market rumors suggested that the first batch of tin ore from Myanmar's Wa region had obtained export licenses (later verified that most miners had not paid fees, and production resumptions fell short of expectations). Spot market transactions for tin ingots: Price declines stimulated restocking. Trading was sluggish at the beginning of the week, with smelters maintaining firm quotes but actual transactions being scarce. Downstream caution: End-users made just-in-time procurement only, with traders reporting "few purchases at current prices, with more transactions based on deferred pricing." Restocking was released after the price decline (May 29). Low prices stimulated demand: After tin prices fell below 260,000 yuan/mt, downstream restocking interest increased amid price dips: Some end-user enterprises made just-in-time procurement, with traders achieving over 100 mt in single-day transactions (compared to a daily average of approximately 20-30 mt previously).

LME tin inventory: LME tin inventory data on May 30 was 2,680 mt, compared to 2,755 mt on April 30. LME tin inventory experienced a slight decline in May, with a decrease of 2.72%.

SMM Outlook

Macro: In the future, attention should be paid to the boosting effect on tin prices from the release of several major financial policies by China at the Lujiazui Forum and whether other stimulus policies will be introduced to boost future demand in the tin market. Additionally, attention should be given to China-US PMI, CPI, PPI, domestic imports and exports, and social financing, as well as US non-farm payrolls data and the guidance of market expectations from the US Fed's June interest rate-setting meeting. Furthermore, it is worth noting that the uncertainty surrounding US tariffs has repeatedly disrupted the market performance of metals such as tin. In the future, attention should also be paid to tariff negotiations between Europe and the US, as well as the US's imposition of tariffs on solar energy from ASEAN.

Fundamentals: In terms of supply: Based on SMM calculations, affected by planned shutdowns for maintenance at some smelters in Yunnan and Jiangxi, refined tin production is expected to continue to decline MoM in June. The Wa region in Myanmar officially resumed production at the end of April 2025, but actual capacity ramp-up has been slow. Affected by earthquakes and infrastructure damage, shipments had only reached 30% of pre-shutdown levels by late May. The approval of new mining licenses has been strict, with actual approved production capacity reduced. Coupled with export tax system reforms (changing from cash tax to in-kind tax), it is expected that China's tin ore imports from Myanmar in 2025 will significantly decline compared to the average from 2019-2022. Although the Bisie mine announced phased production resumptions, the repair of the power system will take more than three months. Despite refined tin exports from Indonesia increasing by over 50% YoY in March and April, license approvals are still affected by corruption investigations, and the government's strengthening of local smelting policies may compress medium and long-term export potential. In summary, the supply recovery in major tin mining regions in 2025 is significantly lower than market expectations, providing support to tin prices from the supply side. On the demand side, influenced by the traditional seasonal consumption off-season in downstream industries, downstream demand for tin remains weak, which will put pressure on tin prices.

In summary, the uncertainty in the overseas macro environment will exacerbate tin price volatility, while the fundamental landscape presents a tug-of-war between "rigid supply shortages" and "seasonal demand weakness" — the slow pace of tin mine production resumptions in Myanmar and the DRC, coupled with declining tin grades in major producing regions, makes it difficult to fill the supply gap, providing price support. However, the off-season effect on the demand side suppresses market performance, and it is necessary to monitor whether downstream restocking demand can continue to be released after tin price corrections. In addition, the progress of tin inventory drawdown both domestically and internationally will also have a phased impact on prices. Going forward, it is crucial to closely monitor the pace of overseas tin mine production resumptions, changes in overseas tin ore imports, and signals of marginal demand improvement under the stimulation of relevant domestic policies.

Recommended readings:

》[SMM Analysis] Operational Analysis and Trend Outlook of China's Refined Tin Industry in May 2025

》Social Inventory of Tin Ingots by Region as of May 30, 2025 [SMM Data]

![The Most-Traded SHFE Tin Contract Opened Lower and Then Traded Stronger, Spot Market Recovers Amid Downtrend [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/WWXJU20251217171753.jpg)

![The most-traded SHFE tin contract fluctuated rangebound during the night session, with downstream enterprises mostly following up with small-lot transactions. [SMM Tin Morning Brief]](https://imgqn.smm.cn/usercenter/bYFQn20251217171752.jpg)